As we prepare to formally wrap up 2025, the big-picture story for the A/E industry largely remains the same. Firms across every discipline, size and geography are churning out yet another strong year of growth, revenue, profitability and backlog. In fact, leaders largely shrugged off the tax, tariff and policy reverberations and instead focused on an emerging 21st-century capex-driven design and construction landscape of AI-led data centers, energy infrastructure and manufacturing hubs. Organizations continued to hire talent at all levels and opened new branch offices everywhere in numbers last seen before the pandemic. And to put an exclamation point on it all, 2025 will mark the best year ever for M&A activity.

When all is said and done, we’ll finish the year with a record for A/E North America transactions, up about 6 percent over 2024’s banner levels. Attractive valuations, exceptional financial performance and competitive pressures have encouraged a huge seller demographic (peak late-stage Baby Boomers) to explore and engage with eager, confident buyers and investors. This vigorous activity has created a bit of industry peer pressure, with other owners and executives waiting on the sidelines to decide which growth or exit path to pursue.

Rampant M&A Has Resulted in Fewer Design Firms

To be sure, the A/E industry has been consolidating for a long time. For more than two decades, an increasing number of owners have decided to “sell out” vs. “sell down,” while growth-hungry buyers scaled significantly by aggressively rolling up firms. And while we remain bullish on the long-term potential of a new generation of entrepreneurs and A/E startups, so far they haven’t kept pace with the number of companies that have outright disappeared through M&A. As such, we’re generating more aggregate U.S. design revenue than ever before but with dramatically fewer firms.

The following chart exhibits the spike in the number of deals during the last eight years:

Every year includes a narrow set of serial buyers that consistently drive a sizable portion of activity, and 2025 was no different. This year, 25 percent of the completed deals were completed by just 20 consolidators, each acquiring four or more firms.

Big Deals … Small Deals

The year was noteworthy not only for the overall number of deals but also for the signature combinations and prominent cross-border activity. In December 2025, WSP made a bold announcement that it would acquire engineering and environmental giant TRC Companies, creating the largest power and energy platform in the United States. Earlier in 2025, publicly traded NV5 joined forces with Acuren to create an 11,000-person integrated engineering, inspection and geospatial organization. Stantec acquired Page, a leading A/E firm, to deepen its expertise and resources in advanced manufacturing, data centers and healthcare. AtkinsRéalis Group acquired a majority stake in the prominent civil engineering consultant David Evans and Associates, while Egis purchased Lochner, a national leader in infrastructure and transportation.

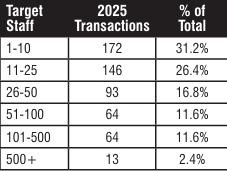

On the other side of the equation, it’s worth remembering that our M&A is really dominated by small sellers, fueled by aging owners with limited internal transition and succession options. Each year, 50 to 60 percent of all transactions involve A/E firms with 25 or fewer staff members, typically producing net revenue of $4-5 million or less. The median-size A/E seller this year was a 22-person firm. The breakout by seller size is illustrated below:

Private Equity Firmly Embedded Across the Industry

The private-equity phenomenon we first wrote about more than four years ago is indeed here to stay. Financial sponsors now control a stake in well more than 100 A/E firms of every size and discipline. Attracted to narratives such as infrastructure renewal, power/energy demands and environmental stewardship, investors have sought out companies—both as true platforms or as part of a “family of brands” model—to recapitalize, scale and eventually sell.

This year, more than 15 new firms have gone the private-equity route, while several A/E firms with first-stage investors have successfully sold to a new financial partner. In addition, many of these platforms remain active bolt-on acquirers. There’s no denying that private equity has contributed to greater liquidity and broader governance options, along with higher valuations across the industry.

Geographic M&A Priorities Are Changing

During the last five to 10 years, CEOs and their corporate-development teams, along with private-equity investors, have been keenly focused on uncovering A/E targets across the south, especially in Texas and Florida. Following a “roads and rooftops” mentality of favorable migration patterns as well as infrastructure and building trends, hundreds of firms across every discipline—power/energy, architecture, environmental, water, land development, surveying and MEP, among others—have been swept up in this region. And while we still feel there are consolidation opportunities widely available in these areas, we’re also witnessing buyers pivot to untapped sections ripe for exploration. States with strong fiscal positions, favorable affordability, tailwinds from industrial reshoring and AI/technology investments, and access to young talent pools are part of this M&A shift.

Dramatic Changes for Set-Aside Firms May Result in More Sellers

There has been an increasing number of set-aside firms (woman-, minority- and disadvantaged-owned businesses) that have sold during the last few years, particularly those that focus exclusively on public works and infrastructure. In October 2025, the U.S. Department of Transportation published an Interim Final Rule in the Federal Register that revises the federal DBE certification process. Other individual states have followed suit.

In 2026, we’ll see final evaluation procedures for narrative-based applications. As a result, countless A/E firms will be required to document individual experiences of disadvantage, and transportation agencies will navigate that transition. Exactly how this will shake out, we don’t know for sure. However, we believe it could prompt some set-aside business owners to explore external sale options to join larger firms that can leverage their staff talent and project experience.

Steve Gido

Steve Gido specializes in corporate financial advisory services, including mergers and acquisitions, business valuations, ownership transition plans, and strategic planning for engineering, architecture, environmental consulting and construction firms. He leads ROG+ Partners’ merger and acquisition practice, and has advised on a wide number of A/E/C transactions, representing buyers and sellers of all sizes and disciplines.

Stormwater Interview with Robert Page, P.E., Vice President, HNTB

TriMet’s Banfield Type 1 Substation Replacement Project

February Issue 2026